The GOP’s Penny-wise, Pound-Foolish Spending Cuts

Let’s say that for every dollar you gave me, I gave you a crisp $10 bill in return. Good deal, right? Almost too good. But before you start to ask questions, I’ll remind you that this is my thought experiment. Perhaps I just love dollar bills. Or perhaps I just love you. At any rate, there are no strings attached, and you can take advantage of it more than once.

Now let’s say that you’re in debt and you need to get your finances in order. Do you start handing me more dollar bills? Or fewer?

If you’ve got any sense, you’ll give me more. Converting dollar bills into $10 bills is an excellent way to pay off your credit card. Except, it seems, if you’re a House Republican.

On March 1, House Republicans voted to cut $600 million from the budget of the Internal Revenue Service for the remainder of 2011, and they want even deeper cuts in 2012. Perhaps that doesn’t surprise you: Republicans don’t like spending — at least when they’re not in power — and they don’t like taxes. Why would they fund the IRS?

Well, as the Associated Press reported, “every dollar the Internal Revenue Service spends for audits, liens and seizing property from tax cheats brings in more than $10, a rate of return so good the Obama administration wants to boost the agency’s budget.” It’s an easy way to reduce the deficit: You don’t have to cut heating oil for the poor or Pell grants for students. You just have to make people pay what they owe.

But deficit reduction is not the GOP’s top priority. It’s a bit lower on the list, somewhere between “get Styrofoam cups back into Congress” — an actual push the Republicans took up to thumb their nose at Nancy Pelosi’s environmental policies — and make “Sesame Street” beg for money. In fact, if you listen to Speaker John Boehner, he’ll tell you himself. “The American people want us to focus on creating jobs and cutting spending,” he has said. And that comment wasn’t a one-off: “Our goal is to cut spending,” he said in another speech.

Cutting spending is related to, but in important ways different from, cutting deficits. For one, it rules out tax increases. That’s how Republicans can lobby to make the Bush tax cuts permanent, at a cost of $4 trillion over 10 years, and yet say they’re fulfilling their campaign promises by making much smaller cuts to non-defense discretionary spending. If you add up what Republicans have offered since the election, the policies they’ve endorsed would increase deficits but also decrease spending, at least in the short term. The IRS example shows that spending cuts don’t always reduce the deficit. But it’s worse even than that: Spending cuts don’t always reduce government spending.

There are three categories of spending in which cuts lead to more, rather than less, spending down the line, says Alice Rivlin, former director of both the Congressional Budget Office and the Office of Management and Budget. Inspection, enforcement and maintenance. The GOP is trying to cut all three.

Let’s begin with the costs of cutting inspection — for example, the Food and Drug Administration and the Agriculture Department. Together, the agencies are charged with ensuring that the nation’s food is safe. That’s increasingly crucial as our interconnected, industrialized system makes contaminated food a national crisis rather than a local problem. In recent years, we’ve seen massive recalls stemming from E. coli in spinach, salmonella in peanut butter and melamine in pet food. Each required the recall of thousands of tons of food and alerts to consumers who, in many cases, were screened or treated.

The problem was bad enough — and the people and pets sick enough— that Congress passed a bipartisan food-safety bill during last year’s lame-duck session. But now Republicans want big cuts in the agencies’ budgets, meaning fewer inspectors and a higher chance of outbreaks and food-borne illness. And those don’t come cheap. They show up in our health-care costs, disability insurance and tax revenue, not to mention in the pain and suffering and even death they cause.

Next up: enforcement. As any budget wonk will tell you, cracking down on “waste, fraud and abuse” won’t cure all our fiscal ills. But waste, fraud and abuse do happen, particularly in Medicare and Medicaid, where they can be costly. Republicans are looking for big reductions in the Department of Health and Human Services, meaning fewer agents to conduct due diligence on health-care transactions. Costs will go up, not down.

Then there’s deferred maintenance. In 2009, the Society of Civil Engineers gave America’s existing infrastructure a grade of D. They estimated that simply maintaining America’s existing stock would require up to $2.2 trillion in investment. But Republicans have been cool to Obama’s calls to increase infrastructure investment. Just “another tax-and-spend proposal,” Rep. John Mica (R-Fla.) said when the initiative was announced. But a dollar in maintenance delayed — or cut — isn’t a dollar saved. It’s a dollar that needs to be spent later. And waiting can be costly. It’s cheaper to strengthen a bridge that’s standing than repair one that’s fallen down.

And there are plenty of examples beyond that. Republicans have proposed massive cuts to the Securities and Exchange Commission, which would make another financial crisis that much likelier. They’ve proposed cuts to the National Oceanic and Atmospheric Administration, which conducts tsunami monitoring. In their zeal to cut spending, they’re also cutting the spending that’s there to prevent overspending. Just as you have to spend money to make money, you also have to spend money to save money — at least sometimes.

There are all sorts of reasons Republicans are being penny-wise and pound-foolish. Cutting $100 billion in spending in one year sounded good on the campaign trail but turned out to be tough in practice. Curtailing the IRS and cutting the Department of Health and Human Services — and, particularly, its ability to implement health-care reform — is a long-term ideological objective for Republicans.

Whatever the reason, the effect will be the same: a higher likelihood of pricey disasters, an easier time for fraudsters, and bigger price tags when we have to rebuild what we could’ve just repaired.

By: Ezra Klein, The Washington Post, March 15, 2011

The Cheaters and Their Banks: Taking The Battle To The Banks

The Obama administration is rightly keeping the pressure on tax cheats and the bank executives who help them by stashing their money in secret accounts overseas. Now we would like to see the Internal Revenue Service and the Justice Department take the battle to the banks themselves. That’s the only way of getting them to drop this lucrative and illegal business.

The Justice Department has charged five bankers with helping wealthy Americans conceal their assets from American authorities. A former employee of Switzerland’s UBS who now works for rival Credit Suisse was arrested in January and accused of helping 100 to 150 Americans hide as much as $500 million from tax authorities.

A few weeks later, three former employees and one current banker at Credit Suisse were indicted for helping 17 Americans conceal assets in accounts at the bank and then helping them move the stash to other banks in Switzerland, Hong Kong and Israel once it was clear American authorities were on the trail of tax evaders at big Swiss banks.

This is a promising route both to recover unpaid taxes and to deter other Americans from trying to evade the I.R.S. this way. So far, however, the banks have faced no charges. The country-hopping by the Credit Suisse account holders in search of a safer hiding place suggests that cross-border tax evasion won’t be shut down until the institutions determine that secret offshore accounts are too risky a business.

The I.R.S.’s strategy gathered momentum when the agency went after UBS, which was caught sending bankers to the United States to offer tax evasion services and settled with the government. The bank paid a $780 million fine and exited the business. It promised to cooperate with the government and later revealed the names of some 5,000 American secret account holders. The case eventually led Switzerland to relax its bank secrecy laws and cooperate with American authorities.

Since then, some 20,000 Americans have disclosed their accounts to the I.R.S., taking advantage of programs that shielded them from prosecution in exchange for paying back taxes, interest and a substantial fine. UBS has since gotten out of the American cross-border banking business, as have Credit Suisse and other big Swiss banks. But there are still banks willing to open secret offshore accounts for wealthy Americans. It will take some more high-profile action against financial institutions to force them out of the racket.

By: The New York Times-Editorial, Opinion Page, March 13, 2011

Another Inside Job: The Continuation Of Banker Bad Behavior

Count me among those who were glad to see the documentary “Inside Job” win an Oscar. The film reminded us that the financial crisis of 2008, whose aftereffects are still blighting the lives of millions of Americans, didn’t just happen — it was made possible by bad behavior on the part of bankers, regulators and, yes, economists.

What the film didn’t point out, however, is that the crisis has spawned a whole new set of abuses, many of them illegal as well as immoral. And leading political figures are, at long last, showing some outrage. Unfortunately, this outrage is directed, not at banking abuses, but at those trying to hold banks accountable for these abuses.

The immediate flashpoint is a proposed settlement between state attorneys general and the mortgage servicing industry. That settlement is a “shakedown,” says Senator Richard Shelby of Alabama. The money banks would be required to allot to mortgage modification would be “extorted,” declares The Wall Street Journal. And the bankers themselves warn that any action against them would place economic recovery at risk.

All of which goes to confirm that the rich are different from you and me: when they break the law, it’s the prosecutors who find themselves on trial.

To get an idea of what we’re talking about here, look at the complaint filed by Nevada’s attorney general against Bank of America. The complaint charges the bank with luring families into its loan-modification program — supposedly to help them keep their homes — under false pretenses; with giving false information about the program’s requirements (for example, telling them that they had to default on their mortgages before receiving a modification); with stringing families along with promises of action, then “sending foreclosure notices, scheduling auction dates, and even selling consumers’ homes while they waited for decisions”; and, in general, with exploiting the program to enrich itself at those families’ expense.

The end result, the complaint charges, was that “many Nevada consumers continued to make mortgage payments they could not afford, running through their savings, their retirement funds, or their children’s education funds. Additionally, due to Bank of America’s misleading assurances, consumers deferred short-sales and passed on other attempts to mitigate their losses. And they waited anxiously, month after month, calling Bank of America and submitting their paperwork again and again, not knowing whether or when they would lose their homes.”

Still, things like this only happen to losers who can’t keep up their mortgage payments, right? Wrong. Recently Dana Milbank, the Washington Post columnist, wrote about his own experience: a routine mortgage refinance with Citibank somehow turned into a nightmare of misquoted rates, improper interest charges, and frozen bank accounts. And all the evidence suggests that Mr. Milbank’s experience wasn’t unusual.

Notice, by the way, that we’re not talking about the business practices of fly-by-night operators; we’re talking about two of our three largest financial companies, with roughly $2 trillion each in assets. Yet politicians would have you believe that any attempt to get these abusive banking giants to make modest restitution is a “shakedown.” The only real question is whether the proposed settlement lets them off far too lightly.

What about the argument that placing any demand on the banks would endanger the recovery? There’s a lot to be said about that argument, none of it good. But let me emphasize two points.

First, the proposed settlement only calls for loan modifications that would produce a greater “net present value” than foreclosure — that is, for offering deals that are in the interest of both homeowners and investors. The outrageous truth is that in many cases banks are blocking such mutually beneficial deals, so that they can continue to extract fees. How could ending this highway robbery be bad for the economy?

Second, the biggest obstacle to recovery isn’t the financial condition of major banks, which were bailed out once and are now profiting from the widespread perception that they’ll be bailed out again if anything goes wrong. It is, instead, the overhang of household debt combined with paralysis in the housing market. Getting banks to clear up mortgage debts — instead of stringing families along to extract a few more dollars — would help, not hurt, the economy.

In the days and weeks ahead, we’ll see pro-banker politicians denounce the proposed settlement, asserting that it’s all about defending the rule of law. But what they’re actually defending is the exact opposite — a system in which only the little people have to obey the law, while the rich, and bankers especially, can cheat and defraud without consequences.

By: Paul Krugman, Op-Ed Columnist, The New York Times, March 13, 2011

What Does The Tea Party Want?….The New Litmus Test

Jim VandeHei and Mike Allen argue that the Tea Party redefined the purpose of the GOP as opposition to spending:

The Republican Party is undergoing a messy but unmistakable 20-month transformation from fanatically anti-Obama to fanatically anti-spending, providing top party officials a new and intriguing playbook for recapturing the White House in 2012.

To understand the current evolution, flash back to late spring of 2009. The GOP was disoriented and adrift, its leadership void filled by the bombastic voices of Palin, Beck and Rush Limbaugh. There was no common conservative cause, beyond fear and loathing of Obama. No wonder swing voters were so down on them.

But the tea party, treated at first by the media as exotics, forced Republicans to focus almost exclusively on the size of government. By the time the 2010 elections rolled around, tea party activists and most independent voters were completely aligned on the need to cut, cut, cut.

Midterm election results showed that this approach offers the GOP its best – and maybe only – hope of keeping the interests of independents and tea party activists aligned enough to beat Obama.

The new litmus tests for GOP presidential hopefuls are support for repealing “Obamacare” and taking a cleaver to government spending. If a presidential candidate could harness the smaller-government conservatism, temper it enough to avoid a blatant overreach and articulate a vision for a prosperous future for the country, it’s not hard to imagine swing voters finding such a person appealing.

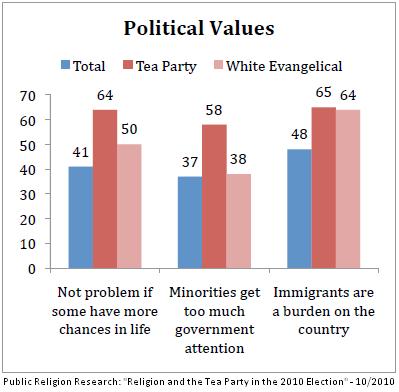

There’s a superficial appeal to this story. But the evidence that Tea Party activists want to cut spending — at least actual spending programs — is sparse. Polls show that Tea Party supports overwhelmingly oppose cuts to Social Security and Medicare. The main thrust of Tea Party opinion is not the belief that Obama has spent too much money, but the belief that Obama has spent too much money on people unlike them:

More than half say the policies of the administration favor the poor, and 25 percent think that the administration favors blacks over whites — compared with 11 percent of the general public.

They are more likely than the general public, and Republicans, to say that too much has been made of the problems facing black people.

Here’s another cut, showing the Tea Party’s greater comfort with inequality of opportunity and stronger belief that the government devotes too many resources to minorities:

It’s a revolt against the composition of government much more than the level.

Now, it’s true that Republicans aren’t exactly translating this blueprint into action, but they’re not exactly flouting it, either. There is always a generalized antipathy toward spending amongst Republican and swing voters, but it disappears when the subject turns to actual government programs. Usually Republicans decide to just cut taxes for the rich instead. Here’s is the one part of the article proposing a defined policy change:

Even Ralph Reed, the Republican operative most tapped in to evangelicals, reflected the new GOP mindset when he gave this surprising wish list for the next presidential race: “In a perfect world, I’d like to hear the Republican nominee run on a platform that takes the capital gains tax to zero over five years.” Reed, who summoned several of the presidential candidates to Iowa for his Faith & Freedom Coalition this week, made it clear that Christian conservatives will still need to be catered to, but added that his side will understand the nominee’s need to focus on swing voters.

So an article putatively about the GOP redefining itself as an anti-spending party has one actual programmatic detail, and it’s: a zeroing out of the capital gains tax. In the name of appealing to swing voters — who, in fact, oppose tax cuts for the rich. Meet the new boss…

By: Jonathan Chait, The New Republic, March 14, 2011

Public Alert: What If We’re Not Broke?

“We’re broke.”

You can practically break a search engine if you start looking around the Internet for those words. They’re used repeatedly with reference to our local, state and federal governments, almost always to make a case for slashing programs – and, lately, to go after public-employee unions. The phrase is designed to create a sense of crisis that justifies rapid and radical actions before citizens have a chance to debate the consequences.

Just one problem: We’re not broke. Yes, nearly all levels of government face fiscal problems because of the economic downturn. But there is no crisis. There are many different paths open to fixing public budgets. And we will come up with wiser and more sustainable solutions if we approach fiscal problems calmly, realizing that we’re still a very rich country and that the wealthiest among us are doing exceptionally well.

Consider two of the most prominent we’re-brokers, House Speaker John Boehner and Wisconsin Gov. Scott Walker.

“We’re broke, broke going on bankrupt,” Boehner said in a Feb. 28 Nashville speech. For Boehner, this “fact” justifies the $61 billion in domestic spending cuts House Republicans passed (cuts that would have a negligible impact on the long-term deficit). Boehner’s GOP colleagues want reductions in Head Start, student loans and scores of other programs voters like, and the only way to sell them is to cry catastrophe.

Walker, of course, used the “we’re broke” rationale to justify his attack on public-worker collective bargaining rights. Yet the state’s supposedly “broke” status did not stop him from approving tax cuts before he began his war on unions and proposed all manner of budget cuts, including deep reductions in aid to public schools.

In both cases, the fiscal issues are just an excuse for ideologically driven policies to lower taxes on well-off people and business while reducing government programs. Yet only occasionally do journalists step back to ask: Are these guys telling the truth?

The admirable Web site PolitiFact.com examined Walker’s claim in detail and concluded flatly it was “false.”

“Experts agree the state faces financial challenges in the form of deficits,” PolitiFact wrote. “But they also agree the state isn’t broke. Employees and bills are being paid. Services are continuing to be performed. Revenue continues to roll in. A variety of tools – taxes, layoffs, spending cuts, debt shifting – is available to make ends meet. Walker has promised not to increase taxes. That takes one tool off the table.”

And that’s the whole point.

Bloomberg News looked at Boehner’s statement and declared simply: “It’s wrong.” As Bloomberg’s David J. Lynch wrote: “The U.S. today is able to borrow at historically low interest rates, paying 0.68 percent on a two-year note that it had to offer at 5.1 percent before the financial crisis began in 2007. Financial products that pay off if Uncle Sam defaults aren’t attracting unusual investor demand. And tax revenue as a percentage of the economy is at a 60-year low, meaning if the government needs to raise cash and can summon the political will, it could do so.”

Precisely. A phony metaphor is being used to hijack the nation’s political conversation and skew public policies to benefit better-off Americans and hurt most others.

We have an 8.9 percent unemployment rate, yet further measures to spur job creation are off the table. We’re broke, you see. We have a $15 trillion economy, yet we pretend to be an impoverished nation with no room for public investments in our future or efforts to ease the pain of a deep recession on those Americans who didn’t profit from it or cause it in the first place.

As Sen. Al Franken (D-Minn.) pointed out in a little-noticed but powerful speech on the economy in December, “during the past 20 years, 56 percent of all income growth went to the top 1 percent of households. Even more unbelievably, a third of all income growth went to just the top one-tenth of 1 percent.” Some people are definitely not broke, yet we can’t even think about raising their taxes.

By contrast, Franken noted that “when you adjust for inflation, the median household income actually declined over the last decade.” Many of those folks are going broke, yet because “we’re broke,” we’re told we can’t possibly help them.

Give Boehner, Walker and their allies full credit for diverting our attention with an arresting metaphor. The rest of us are dupes if we fall for it.

By: E. J. Dionne, Op-Ed Columnist, The Washington Post, March 14, 2011

Share This Blog

Unknown Feed

Unknown Feed- An error has occurred; the feed is probably down. Try again later.

{kind=link}

{kind=link}

You must be logged in to post a comment.